SNB rate cut of 19 June 2025

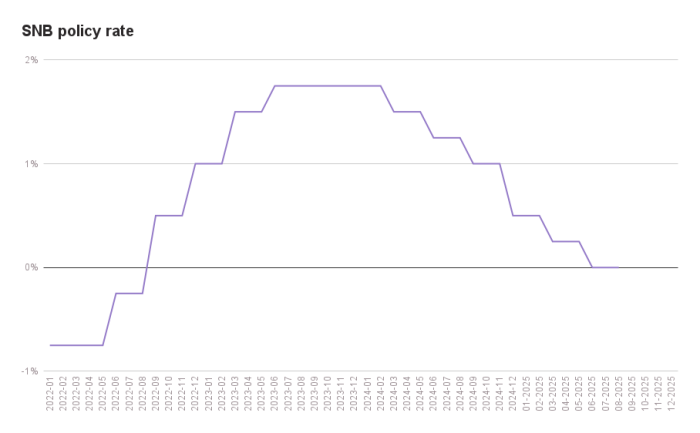

On 19 June 2025, the Swiss National Bank (SNB) cut its key interest rate by 25 basis points, bringing it down to 0%. This move, widely anticipated by both market participants and analysts, aligns with the baseline scenario most experts had forecast.

The decision was primarily driven by the recent drop in inflation. In May, Swiss inflation turned negative for the first time in four years, coming in at -0.1%. This decline in price levels reinforced the SNB's view that a rate cut was appropriate to maintain price stability.

The SNB emphasized that the monetary easing is a response to subdued inflationary pressure and confirmed it will continue to monitor economic developments closely. The central bank stands ready to adjust its monetary policy stance if needed to ensure inflation remains within the price stability range over the medium term.

Inflation Decline Supports Monetary Policy Easing

The June rate decision was enabled by persistently declining inflation over recent months. In May, consumer prices fell into deflationary territory at -0.1%, compared to 0.3% at the time of the previous policy decision. According to the SNB, this decrease was largely driven by falling prices in the tourism sector and for petroleum products.

The SNB also published a revised conditional inflation forecast, which is lower than the projections from its previous decision. Inflation is now expected to average 0.2% in 2025, 0.8% in 2026, and 0.7% in 2027. Notably, these forecasts are based on the assumption of the current interest rate path. Without the latest rate cut, inflation would have been projected to fall even further.

What Is the SNB/BNS’s Conditional Inflation Forecast?

Under Swiss law, maintaining price stability is the Swiss National Bank’s (SNB) primary mandate. Inflation trends are therefore the most important factor in assessing the monetary policy stance. When trade-offs arise, price stability takes precedence over economic growth or exchange rate considerations.

The SNB’s conditional inflation forecast is the central tool for evaluating monetary policy. In simple terms: the SNB selects the interest rate that will most likely keep inflation within its target range over the forecast horizon.

Markets Priced in the Rate Cut in Advance

Ahead of the rate decision, markets had already priced in a rate cut of 32 basis points—meaning that interest rates had evolved as if the SNB were to lower the policy rate by that amount on 19 June. Short-term interest rates, which are more directly influenced by changes in the policy rate than long-term rates, declined significantly over the past two months, serving as a clear signal that markets were expecting a rate cut.

Economic Outlook Before the SNB Decision

The Swiss State Secretariat for Economic Affairs (SECO) has recently revised its economic forecast downward—to 1.3% growth for 2025 and 1.2% for 2026. These figures point to significantly below-average growth for the Swiss economy, despite strong performance in the first quarter. However, as stated by SECO and the SNB, that early-year growth was largely driven by front-loading effects: companies rushed to export as much as possible ahead of new US tariffs.

Going forward, economic prospects are difficult to predict and will largely depend on geopolitical developments—especially whether current tensions related to US tariffs escalate or move toward de-escalation.

Strength of the Swiss Franc

The Swiss franc has appreciated recently, particularly against the U.S. dollar. The SNB’s decision to cut rates on 19 June is expected to counteract that trend.

This comes at a politically opportune time. While the SNB could intervene in foreign exchange markets to influence the exchange rate, doing so is particularly challenging in the case of the U.S. dollar. Unlike smaller currencies, the dollar is more resistant to direct intervention due to its high global trading volume.

Tensions between Switzerland and the U.S. over trade policy also make FX interventions a delicate issue. Switzerland is currently on a U.S. watchlist for potential currency manipulation. Further foreign exchange interventions could seriously undermine Switzerland’s negotiating position in ongoing trade discussions.

Impact of the SNB Rate Cut on the Real Estate Market

Fixed-Rate Mortgage Rates

Fixed mortgage rates are composed of swap rates plus a margin. Swap rates reflect market expectations for interest rate developments over a given term (e.g. 2, 5, or 10 years). The SNB’s policy rate directly affects short-term swap rates and indirectly influences long-term ones. In the case of long-term rates, inflation expectations and the broader economic outlook also play a significant role.

The SNB’s decision on 19 June is expected to have only a limited effect on fixed-rate mortgage rates. This is because the rate cut was widely anticipated and had already been priced into current rates. However, if the SNB were to lower its policy rate below zero later this year—or if markets were to expect such a move—fixed mortgage rates could decline further.

SARON Mortgage Rates

The SARON (Swiss Average Rate Overnight) reflects short-term money market rates and typically remains close to the SNB’s current policy rate. A SARON mortgage is priced based on the SARON—subject to a minimum of 0% if rates are negative—plus a contractually agreed margin.

As a result of the 19 June rate cut, SARON mortgage rates will fall one last time. However, the drop in SARON mortgage costs may be smaller than the policy rate cut itself, as many banks are currently increasing their margins. If a bank raises its margin while the policy rate falls, the overall mortgage rate will decline less sharply than the policy rate.

Supply and Demand Dynamics

The SNB’s latest rate cut is set to boost housing demand on multiple fronts. Lower financing costs and the growing appeal of real estate as an investment asset are driving a surge in buyer interest—a trend that has already been emerging in recent months.

Lower financing costs motivate buyers: A lower policy rate translates into reduced mortgage interest rates. For homebuyers, this means lower monthly interest payments, making homeownership more affordable than it was just a few months ago. Unlike existing homeowners—who are often locked into long-term fixed-rate mortgages—new buyers benefit immediately, as they are just now entering the mortgage market. This shift makes homeownership not only more attainable but also more attractive when compared to renting.

Real estate gains appeal as an investment: Another key driver of demand lies in developments on the capital markets. Falling interest rates also mean lower returns on traditional safe investments like government bonds or savings accounts. As a result, real estate is becoming a more compelling alternative for many investors—whether for personal use or as an income-generating asset.

Surge in demand since the beginning of the year: Following last year’s rate cuts, we’ve seen around 70% more active property seekers on our online platform since the start of this year, compared with the same period last year. Today’s policy rate cut is likely to reinforce this trend and lead to a further rise in buyer activity.

Real Estate Prices

The SNB’s rate cut is likely to provide further upward momentum for property prices in Switzerland. Despite the interest rate hikes between 2022 and 2023, real estate prices have continued to rise steadily in recent years. This upward trend is expected to persist into 2025.

The explanation is straightforward: as mortgage rates fall, the purchasing power of prospective buyers increases due to lower monthly financing costs. This leads to higher demand. A larger pool of interested buyers typically allows sellers to ask—and receive—higher prices.

Additional Price Drivers Beyond Interest Rates

Falling mortgage rates contribute to rising real estate prices, but they are not the sole driver. Studies show that the most significant long-term factor is in fact population growth. A growing population, combined with limited housing stock and land availability, leads to a structural shortage. This supply pressure fuels price increases, regardless of interest rate movements.

Moreover, economic performance and inflation also have a statistically greater impact on property prices than interest rates alone. When the economy expands and inflation rises, real estate prices tend to follow suit, amplifying price dynamics beyond the effect of monetary policy alone.

What Buyers and Homeowners Need to Know

Implications for Existing Homeowners

Homeowners with SARON mortgages: The latest rate cut brings good news for those with SARON-linked mortgages. Their interest payments will decrease once again, further reducing monthly financing costs.

Homeowners with fixed-rate mortgages: Those with existing fixed-rate mortgages won’t benefit immediately. However, if you’re already considering refinancing, now could be a good time to explore your options and lock in a favorable rate while conditions remain attractive.

Implications for Prospective Buyers

Lower borrowing costs, depending on mortgage type: SARON mortgages will become even more affordable following the SNB’s decision. Fixed-rate mortgages, by contrast, will see little immediate change, as the rate cut was already priced in by the market. Mortgage rates may fall further if the SNB cuts its policy rate below zero or if markets begin to anticipate such a move.

More properties on the market—but also more buyers: As financing becomes cheaper and inflation remains low, more homeowners are inclined to sell, increasing the supply of properties. At the same time, buyer interest is also on the rise, intensifying competition in the market.

Property search remains challenging: Despite a more favorable interest rate environment, buying a home remains difficult in many regions due to high prices and limited supply.

Affordability rules remain unchanged: While lower mortgage rates reduce the actual cost of homeownership, they don’t affect your ability to qualify for a mortgage. That’s because banks still assess affordability using a hypothetical interest rate of 4.5–5%. So if you didn’t qualify before, you likely still won’t—even with lower market rates.

Implications for Sellers

More homeowners may opt to sell: With stronger demand, many owners are increasingly open to selling their properties.

Prices expected to rise: With more buyers in the market, sellers are in a stronger negotiating position, and can generally push for higher asking prices.

Faster sales possible: Increased demand may result in quicker transactions—although this effect may be offset if sellers also raise their price expectations.