SNB Interest Rate as of March 20, 2025

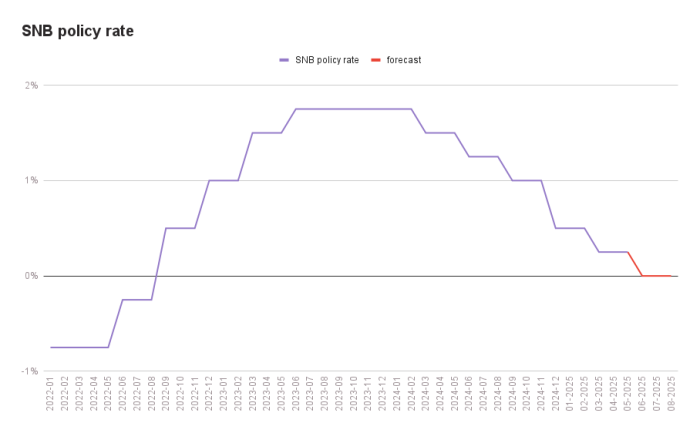

As widely expected, the SNB has opted for a moderate approach, cutting its key interest rate by 25 basis points to 0.25%. The move aims to keep monetary conditions aligned with the current low inflationary pressure. The SNB stated that it will continue to monitor the situation closely and adjust its policy if needed to maintain price stability in the medium term.

SNB Interest Rate March 2025. Source: SNB.

Declining Inflationary Pressure

The latest rate cut was largely expected, as inflationary pressure has eased further since the last decision. In February, inflation fell to just 0.3%, down from 0.4% in January and 0.6% in December.

According to the SNB, the drop from 0.7% to 0.3% is mainly due to lower electricity prices in January. Domestic service costs, on the other hand, continue to be the main contributor to inflation.

The SNB’s updated inflation forecast has barely changed compared to the last decision. The SNB now projects inflation at 0.4% for 2025 and 0.8% for 2026 and 2027. However, the central bank cautioned that economic and inflation forecasts remain highly uncertain due to ongoing trade and geopolitical tensions.

Rising Long-Term Interest Rates

At the time of the last SNB decision, long-term mortgage rates were at a three-year low. However, the interest rate environment has since shifted. Swap rates—the reference for long-term mortgage rates—have risen significantly. The main driver of this increase is heightened uncertainty in the financial markets, particularly concerns over the economic impact of Trump’s trade policies. Investors are demanding higher risk premiums for long-term investments, pushing swap rates higher.

This trend is already affecting the mortgage market. As banks face higher financing costs, they are passing them on to borrowers through increased mortgage rates. Since the last SNB interest rate cut, long-term fixed mortgage rates have climbed, though they remain well below their 2022–2023 peak.

The latest SNB rate cut is expected to have only a minor impact on mortgage rates. SARON mortgages and short-term fixed-rate mortgages may see a slight reduction, but long-term fixed rates are unlikely to change much, as the cut was already factored into market expectations.

Will Negative Interest Rates Return?

With the SNB lowering its key rate to 0.25%, speculation about a possible return to negative interest rates is growing. While many believed the era of negative rates had ended with the global rate hikes after 2022, the SNB has never ruled them out entirely.

The likelihood of a return to negative rates depends on several factors. Inflation in Switzerland currently sits at 0.3%, well within the SNB’s target range of 0–2%, meaning there is little urgency for further easing. However, if a deflationary shock were to hit the economy, forcing the SNB to prioritize economic stimulus, a return to negative rates could become a real possibility.

Less Pressure on the Swiss Franc

One factor working in the SNB’s favor is that pressure on the Swiss franc has eased slightly. Back in December, the franc was at record highs due to rate cuts in the Eurozone and the U.S., which made euro- and dollar-denominated investments less attractive and led investors to seek safety in the franc.

However, recent developments in Europe have shifted the dynamic. The EU is ramping up military spending, and Germany is rolling out a new debt package. These measures are inflationary, leading to higher interest rates in the Eurozone, which makes the euro more appealing and eases the upward pressure on the Swiss franc.